Inventory

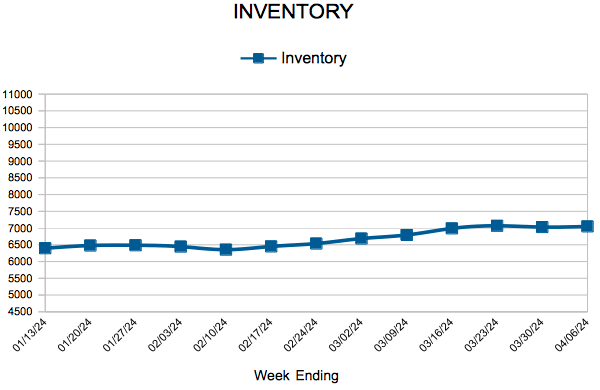

For Week Ending April 6, 2024

For Week Ending April 6, 2024

The share of homebuyers who paid cash for their home reached a 10-year high recently, according to the National Association of REALTORS®, with cash buyers accounting for 32% of all home purchases in January. Real estate investors and vacation-home buyers made up the majority of cash buyers during the past 6 months; among those consumers who paid cash for a home purchase last year, 26% were repeat buyers, while just 6% were first-time buyers.

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING APRIL 6:

FOR THE MONTH OF FEBRUARY:

All comparisons are to 2023

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

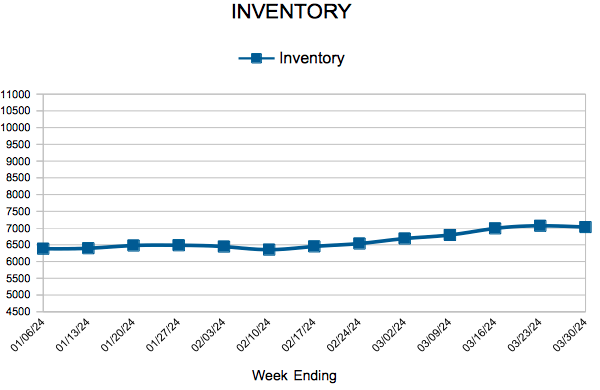

For Week Ending March 30, 2024

For Week Ending March 30, 2024

U.S. residential housing starts jumped 10.7% from the previous month to a seasonally adjusted annual rate of 1.521 million units, led by a surge in single-family starts, which increased 11.6% to 1.129 million units from the previous month, according to the U.S. Census Bureau. Meanwhile, overall housing completions rose 19.7% to a seasonally adjusted annual rate of 1.729 million units, the highest level since January 2007.

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING MARCH 30:

FOR THE MONTH OF FEBRUARY:

All comparisons are to 2023

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

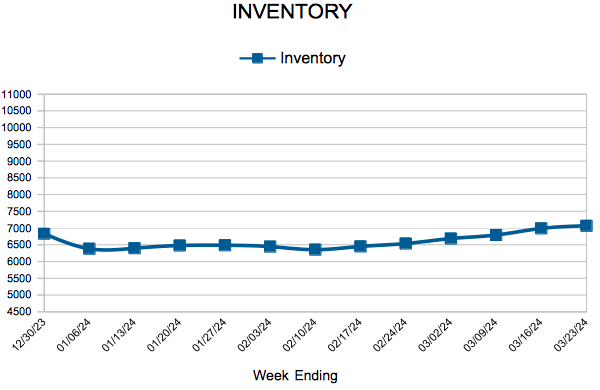

For Week Ending March 23, 2024

For Week Ending March 23, 2024

Housing inventory continues to improve nationwide, climbing 14.8% year-over-year according to Realtor.com’s February 2024 Monthly Housing Market Trends Report. New listings increased 11.3% year-over-year, while the total number of unsold homes rose 8.8% compared to the same period last year. Of particular note was the rise in inventory of homes in the $200,000 to $350,000 price range, which grew 20.6% annually, outpacing all other price categories.

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING MARCH 23:

FOR THE MONTH OF FEBRUARY:

All comparisons are to 2023

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.