New Listings and Pending Sales

Lakeville Real Estate

For Week Ending February 4, 2023

For Week Ending February 4, 2023

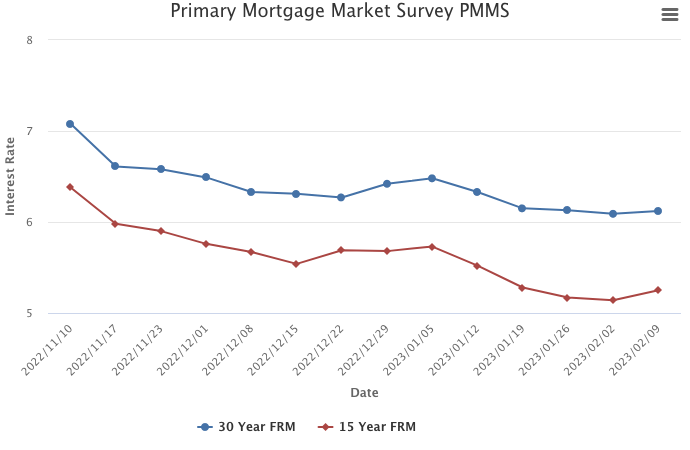

Mortgage rates continued their downward trend, with the 30-year fixed-rate mortgage averaging 6.09% the week ending 2/2/23, according to Freddie Mac. Mortgage rates have declined steadily for the past 4 weeks and are now at their lowest level since their peak in November, when rates hit 7.08%. The drop in rates could save homebuyers hundreds of dollars on their monthly mortgage payments and may provide a boost in home sales ahead of the spring selling season.

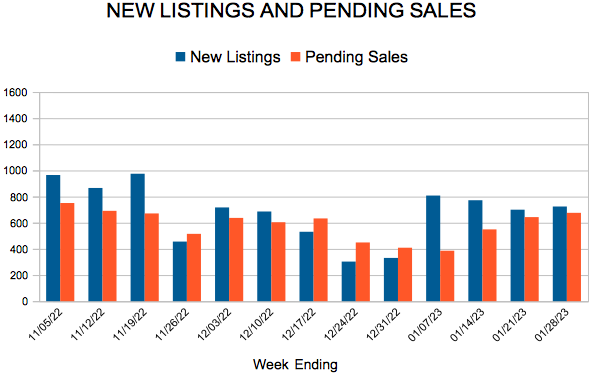

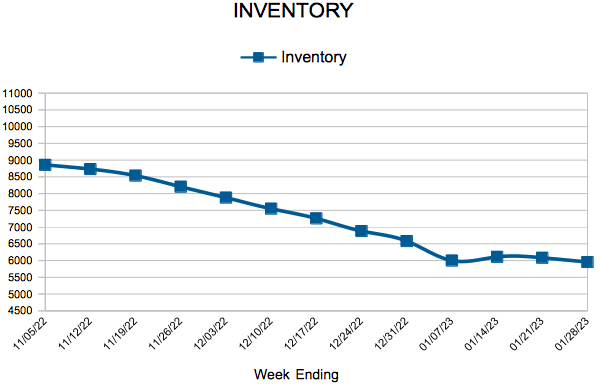

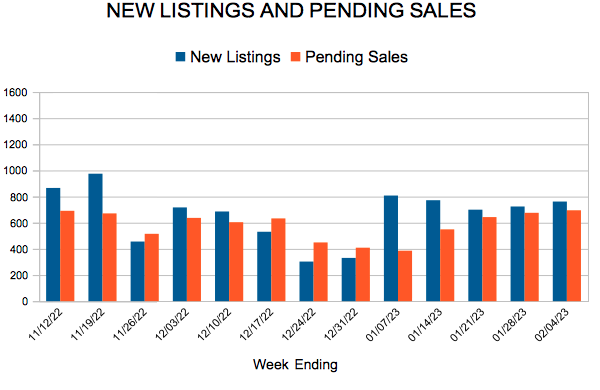

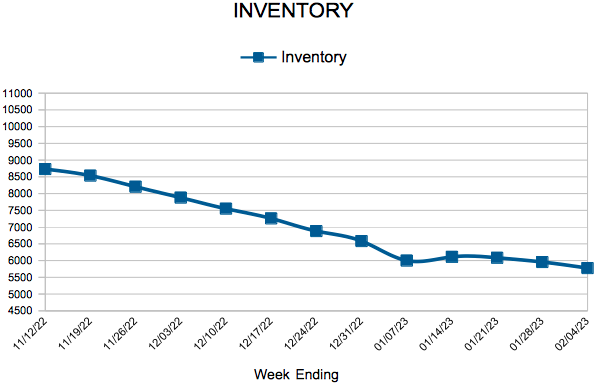

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING FEBRUARY 4:

FOR THE MONTH OF DECEMBER:

All comparisons are to 2022

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

February 9, 2023

Following an interest rate hike from the Federal Reserve and a surprisingly strong jobs report, mortgage rates increased slightly this week. The 30-year fixed-rate continues to hover close to six percent, and interested homebuyers are easing their way back to the market just in time for the spring homebuying season.

Information provided by Freddie Mac.