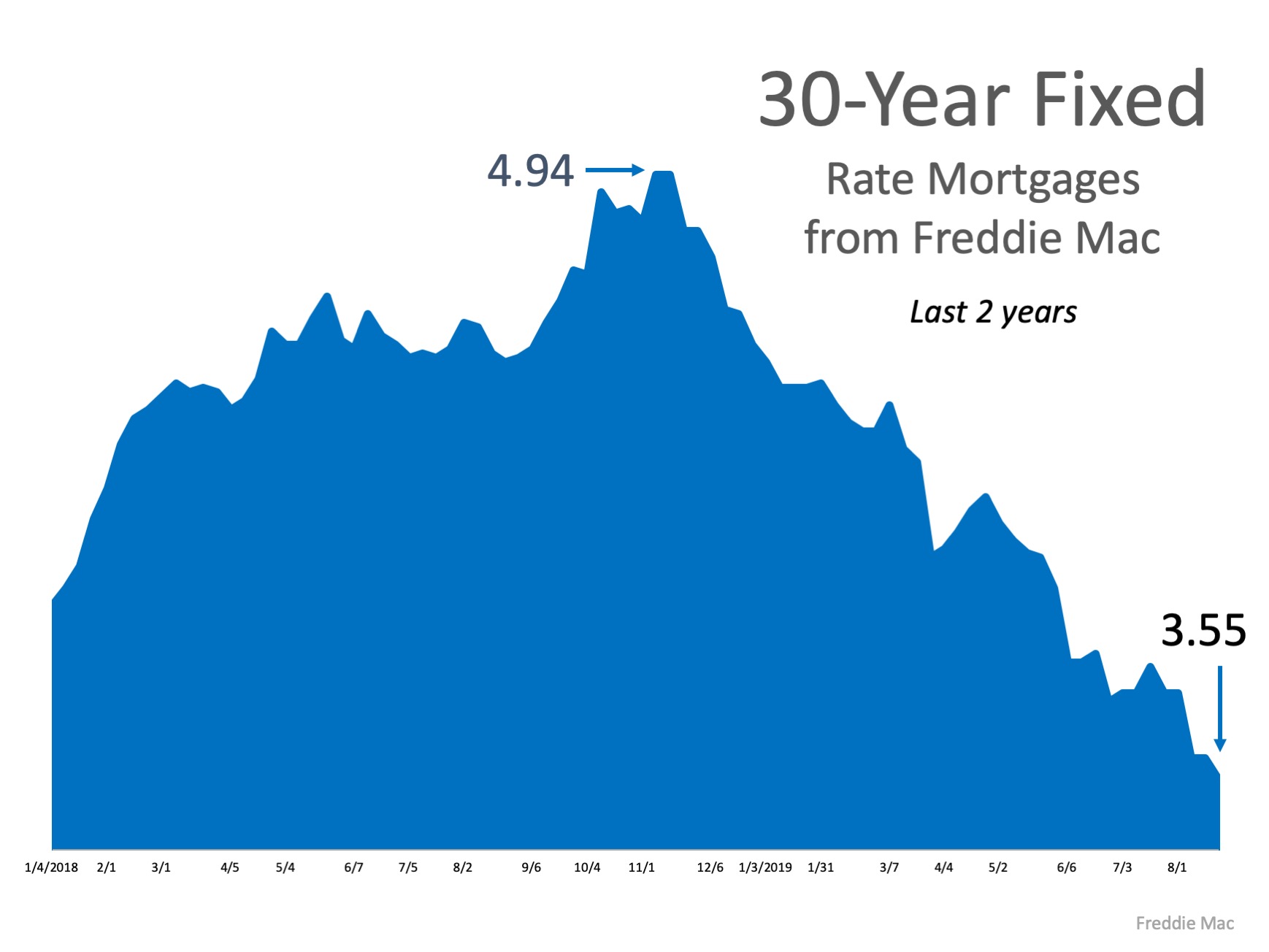

Freddie Mac, Fannie Mae, and the Mortgage Bankers Association are all projecting home sales will increase nicely in 2020.

Below is a chart depicting the projections of each entity for 2019, as well as for 2020. As we can see, Freddie Mac, Fannie Mae, and the Mortgage Bankers Association all believe homes sales will increase steadily over the next year. If you’re a homeowner who has considered selling your house recently, now may be the best time to put it on the market.

As we can see, Freddie Mac, Fannie Mae, and the Mortgage Bankers Association all believe homes sales will increase steadily over the next year. If you’re a homeowner who has considered selling your house recently, now may be the best time to put it on the market.

![A Recession Does Not Equal a Housing Crisis [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2019/08/29062756/2019830-Share-KCM-549x300.jpg)

![A Recession Does Not Equal a Housing Crisis [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2019/08/29061711/20190830-MEM.jpg)