![2020 Homebuyer Preferences [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2020/08/06152056/20200807-KCM-Share-549x300.jpg)

![2020 Homebuyer Preferences [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2020/08/06152053/20200807-MEM.jpg)

Some Highlights

- A recent study from HarrisX shows the current health crisis isn’t slowing down today’s homebuyers.

- Many buyers are accelerating their timelines to take advantage of low mortgage rates, and staying home has enabled some to save more money to put toward a down payment.

- Let’s connect today if your needs have recently changed and you’re ready to make a move this year.

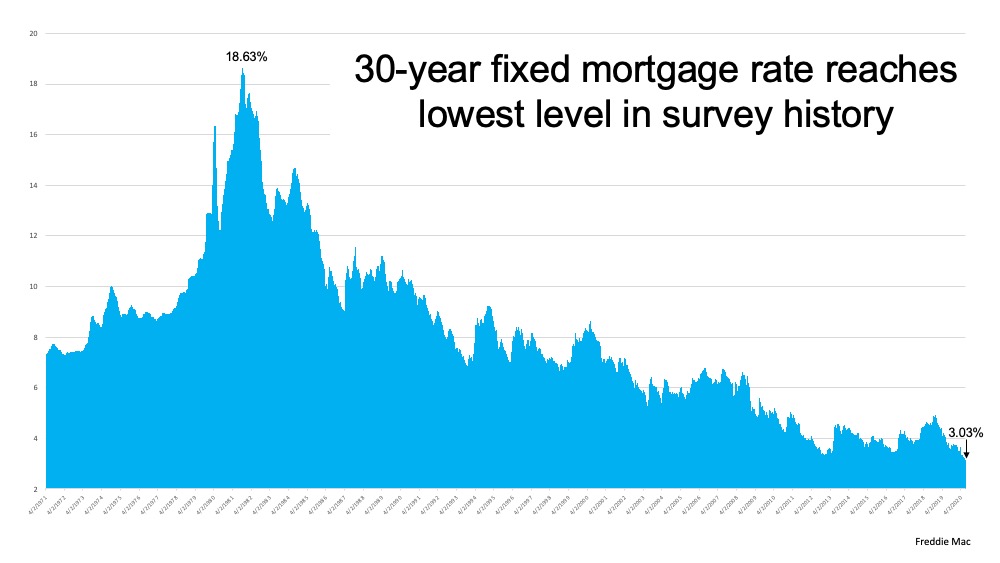

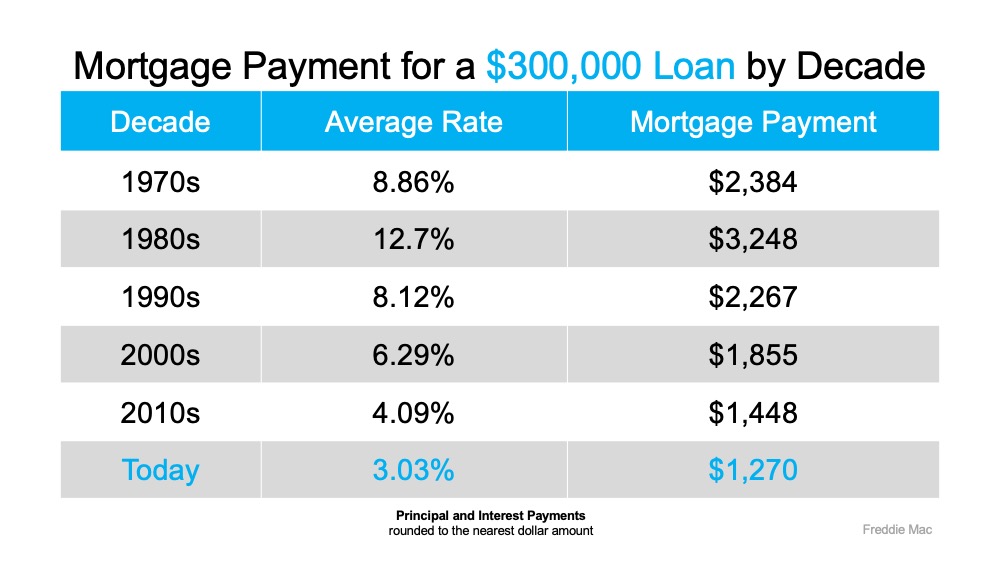

![Mortgage Rates Fall Below 3% [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2020/07/16182030/20200717-Share-571x300.jpg)

![Mortgage Rates Fall Below 3% [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2020/07/16175502/20200717-MEM.jpg)