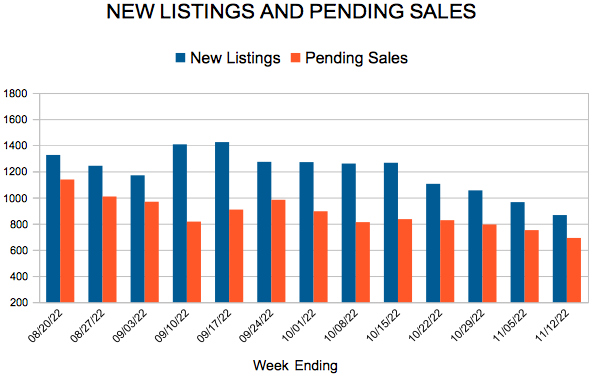

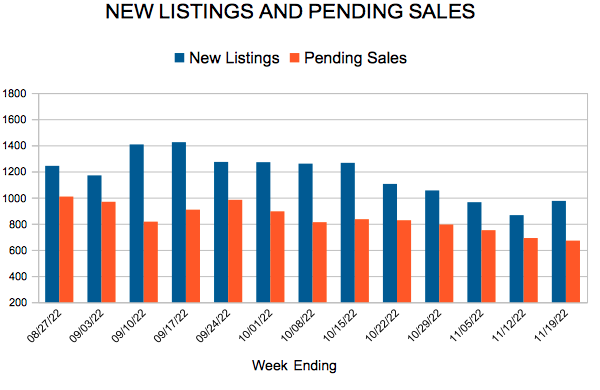

New Listings and Pending Sales

Lakeville Real Estate

For Week Ending November 19, 2022

For Week Ending November 19, 2022

Housing supply continues to grow nationwide, as higher borrowing costs cause home sales to slow. According to Realtor.com’s Monthly Housing Market Trends Report, the national inventory of active listings increased 33.5% year-over-year in October, the highest inventory level since 2020. As a result, local buyers may find they have more options to choose from, and with homes spending more days on market compared to the same period last year, a bit more time to shop around as well.

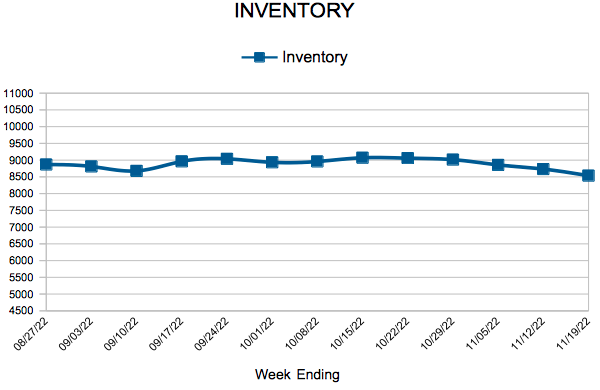

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING NOVEMBER 19:

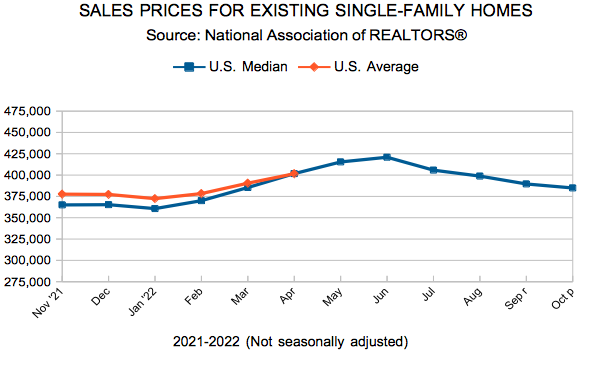

FOR THE MONTH OF OCTOBER:

All comparisons are to 2021

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

November 23, 2022

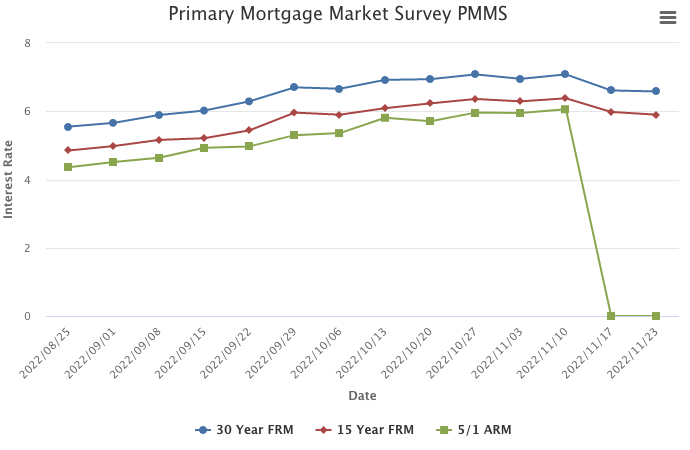

Mortgage rates continued to tick down heading into the Thanksgiving holiday. In recent weeks, rates have hit above seven percent only to drop by almost half a percentage point. This volatility is making it difficult for potential homebuyers to know when to get into the market, and that is reflected in the latest data which shows existing home sales slowing across all price points.

Information provided by Freddie Mac.