The largest obstacle renters face when planning to buy a home is saving for a down payment. This challenge is amplified by rising rents, which has eaten into the amount of money renters have leftover for savings each month after paying expenses.

In combination with higher rents, survey after survey has shown that non-homeowners (renters and those living rent-free with family or friends) believe they need to save upwards of 20% for their down payment!

According to the “Barriers to Accessing Homeownership” study commissioned in partnership between the Urban Institute, Down Payment Resource, and Freddie Mac, 39% of non-homeowners and 30% of those who already own a home believe they need more than a 20% down payment.

The percentage of those who are aware of low down payment programs (those under 5%) is surprisingly low at 12% for non-homeowners and 13% for homeowners.

In a recent Convergys Analytics report, they found that 49% of renters believe they need at least a 20% down payment.

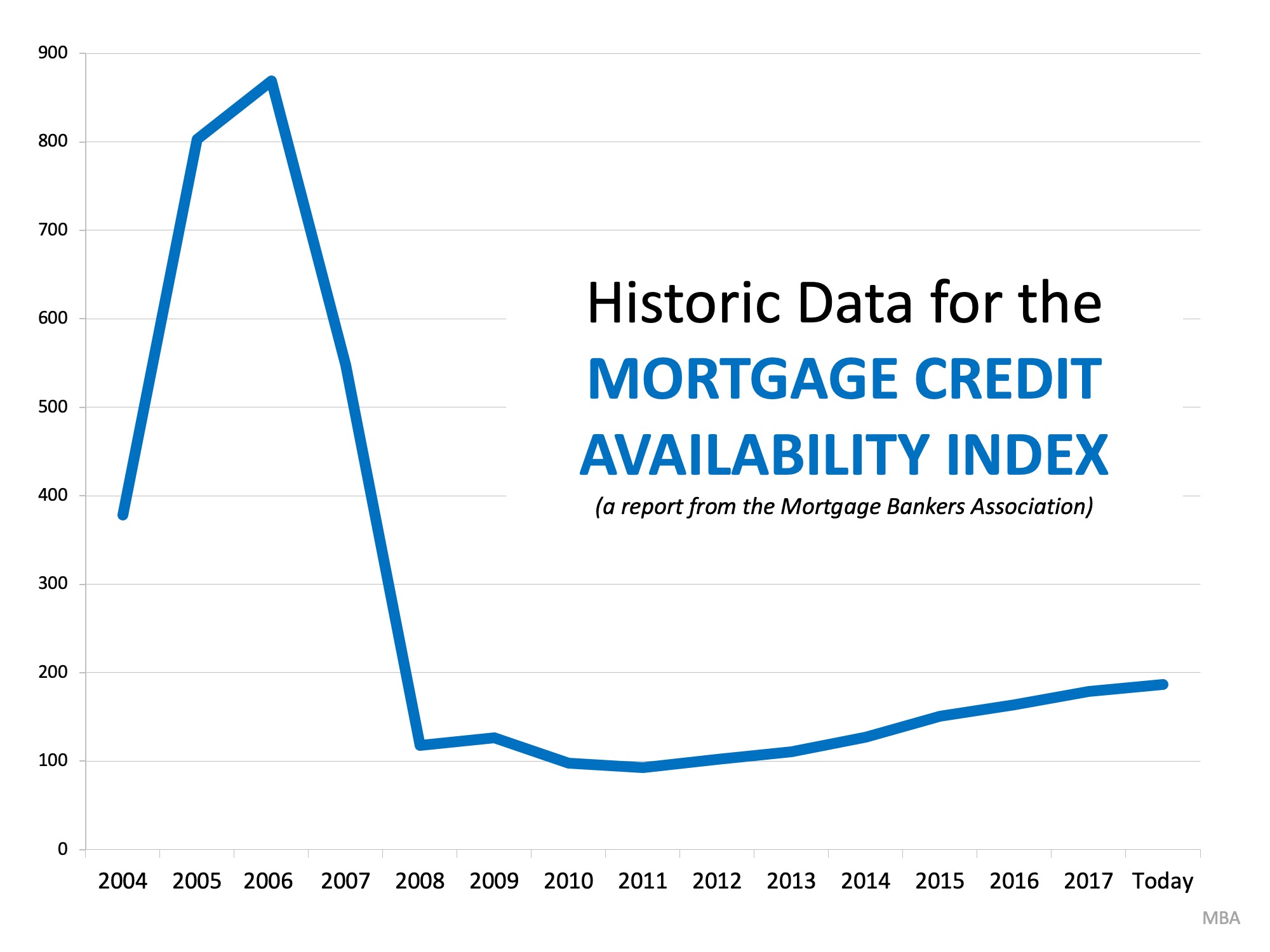

The median down payment on loans approved in 2018 was only 5%! Those waiting until they have over 20% may already have enough saved to buy now!

There are over 45 million millennials (33%) who are mortgage ready right now, meaning their income, debt, and credit scores would all allow them to qualify for a mortgage today!

Bottom Line

If your five-year plan includes buying a home, let’s get together to determine what it will take to make that plan a reality. You may be closer to your dream than you realize!

![The Cost of Renting vs. Buying a Home [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2018/11/06150902/20181116-ENG-STM.jpg)