February 10, 2022

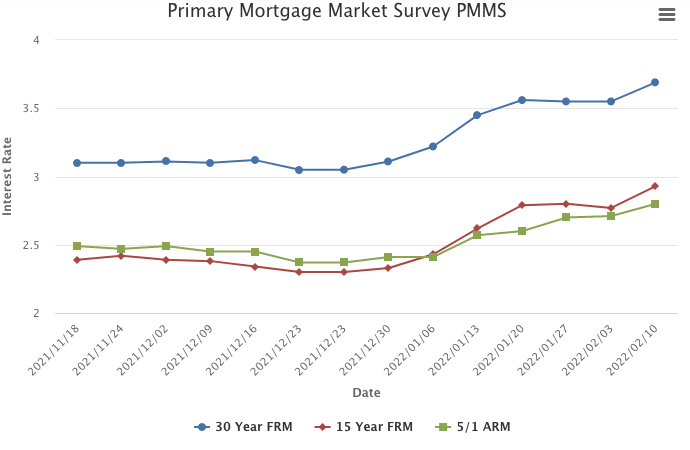

The normalization of the economy continues as mortgage rates jumped to the highest level since the emergence of the pandemic. Rate increases are expected to continue due to a strong labor market and high inflation, which likely will have an adverse impact on homebuyer demand.

Information provided by Freddie Mac.